Lengthy Time period Monetary Objectives to Safe Your Monetary FutureLong-Time period Monetary Objectives: How To Plan Your Monetary Future at Any Age

Lengthy-term monetary objectives take 5 or extra years to perform and usually apply to main life occasions. Among the most necessary long run monetary objectives individuals have embrace saving for retirement and paying off their mortgage.

It’s pure to really feel overwhelmed when serious about your funds a number of years down the street. Seeing your accountability for a mortgage, bank card debt, or private mortgage can typically really feel unmanageable when seen as a complete. The important thing to overcoming this sense is to organize your self lengthy earlier than the necessity arises. Setting long-term monetary objectives early in life could make the method extra manageable.

Lengthy-term monetary objectives take 5 or extra years to perform and usually apply to main life occasions. In addition: You may set them anytime in your life. This information breaks down the right way to set a long-term monetary purpose at any stage of your life and supplies tangible monetary purpose examples to encourage your planning.

Why Are Lengthy-Time period Monetary Objectives Necessary?

For those who solely deal with monetary objectives related to your present scenario, it’s possible you’ll end up unprepared whenever you expertise future life occasions. For instance, saving an emergency fund is an extremely helpful short-term purpose, however should you don’t lower your expenses exterior of that fund, then you’ll be unprepared for retirement. Lengthy-term monetary objectives convey consciousness to occasions which may be many years away and assist to make sure you’ll be ready for after they arrive.

Lengthy-Time period vs Brief-Time period Monetary Objectives

Whereas long-term monetary objectives deal with a number of years into the longer term, short-term objectives are involved with the current. Brief-term objectives can usually be completed inside a 12 months and are often simple to realize. Typical short-term monetary objectives embrace establishing a month-to-month price range and saving an emergency fund. Establishing key short-term objectives may also help buyers obtain their long-term cash objectives by getting them heading in the right direction early on.

Lengthy-Time period vs Mid-Time period Monetary Objectives

Mid-term monetary objectives are a grey space in monetary planning. They typically overlap with quick and long-term objectives—taking longer to realize than short-term objectives, whereas easier than long-term objectives. Saving for a down cost can fall underneath both sort of economic purpose because the quantity it’s essential save can differ primarily based on the dimensions of the acquisition. It may take greater than 5 years to save lots of up for a home down cost relying in your revenue and the price of the home.

Lengthy-Time period Monetary Objectives For Your 20s

Your 20s symbolize a singular time in your monetary journey since many individuals begin out with a clean web page. Figuring out the place to start generally is a problem, however this time in your life has the facility to set the stage for many years to return. Setting monetary objectives now can enhance your high quality of life and reply the query, “The place ought to I be financially at 25?”

Determine Your Retirement Wants

Though your retirement is probably going a number of many years away, figuring out your future wants will improve your probability of assembly them after they come up.

Take into consideration seemingly bills you’ll have presently in your life. How a lot would possibly you obtain from social safety? Will you’ve gotten lease or mortgage funds? How a lot will it’s essential obtain out of your retirement account to cowl your estimated retirement price range?

You may construct your present month-to-month financial savings plan round your anticipated future wants. Evaluating these must your present revenue will show you how to decide if these objectives are lifelike and if it’s essential discover new revenue streams.

Open a Retirement Account

Saving cash early on is the one of many best methods to safe your monetary future. The curiosity you earn in your financial savings will compound, resulting in exponential progress by the point you’re able to withdraw it. The rule of thumb is to save lots of 15 % of your pre-tax revenue every year.

There are a number of choices for the place to take a position your cash. A few the most typical embrace particular person retirement accounts(IRA) and 401(ok)s. It may be very useful to take part in your employer’s retirement program since they typically embrace firm contributions, which is like an addition to your wage.

Save For a Home Down Fee

Most individuals dream of proudly owning property. Constructing fairness in an appreciating asset as an alternative of spending cash on lease might be an effective way to get rid of future bills after you repay the mortgage.

The amount of cash it’s essential save might be dependent upon the price of your required residence. A down cost of 20 % can decrease your rate of interest and get rid of the necessity for personal mortgage insurance coverage (PMI). If your required first residence prices $300,000, then you will want a down cost of $60,000 to satisfy this requirement. Smaller down funds are potential, however they are going to have an effect on your rate of interest and the probability of being permitted for the mortgage.

Pay Off Credit score Card Debt

Bank cards can permit you fast entry to funds whenever you want them most, however carrying bank card debt can shortly wipe out your monetary progress. In an ideal world, you’ll be paying off your bank card month-to-month with out accruing any curiosity.

Within the occasion that you’ve got collected bank card debt, it must be a prime precedence to pay it off. Excessive rates of interest, typically surpassing 15 %, offset the good points you’d be making by investing that very same cash whereas holding the debt. Use a bank card payoff calculator to learn the way lengthy it’ll take to settle your debt.

Enhance Your Earnings Potential

Making more cash is the straightforward reply to securing your monetary future, however how do you go about making it occur? Evaluating the place you wish to be in 5 years is a good start line. Does your profession path require the next stage of schooling than you presently have? Does your present job have a glass ceiling stopping progress?

Speak to your boss about your aspirations. There could also be coaching they will suggest to place you on the ladder of success. In case your present employer is unable or unwilling to assist, take into account upskilling by yourself. Get certifications independently or enter a graduate program. Proactively discovering methods to extend your earnings is best than losing years at a dead-end job.

Lengthy-Time period Monetary Objectives For Your 30s

Getting into your 30s typically brings a brand new diploma of stability to your funds. Ideally, you’ll be on a profession path that means that you can meet many of the long-term monetary objectives you set for your self in your 20s. Nonetheless, with age comes life adjustments which will require you to shift your priorities.

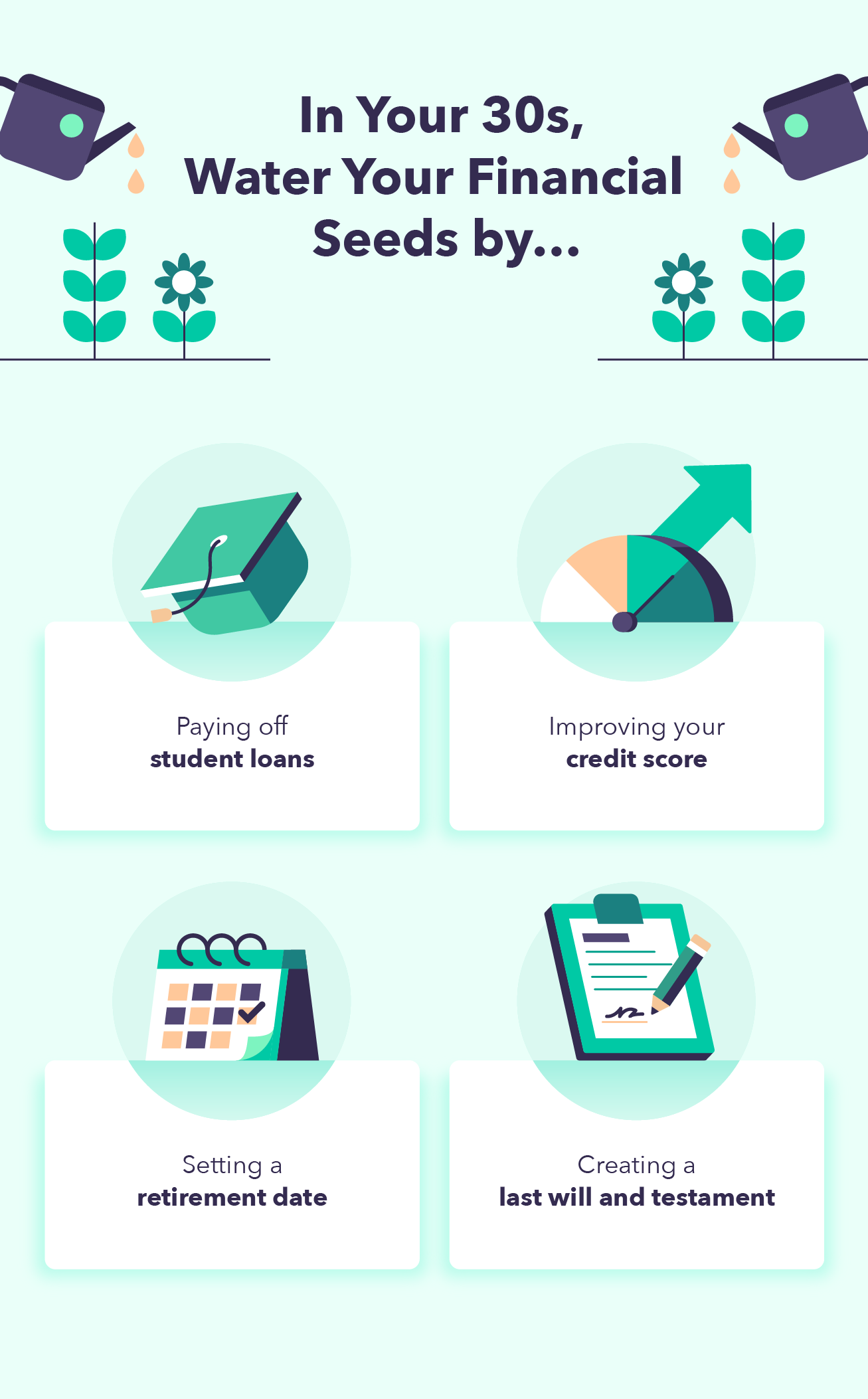

Pay Off Pupil Loans

The earlier you repay your money owed, the more cash you possibly can put towards different monetary objectives. When you have no greater commitments, it may be higher to aggressively repay your scholar loans early. Variable loans could also be manageable for you in the meanwhile, but when rates of interest rise, your mortgage might shortly improve by greater than 5 %.

Massive funds aren’t a risk for each investor’s objectives. Placing simply 10 % of your gross revenue towards your scholar loans can nonetheless be sufficient to whittle away your excellent debt. As your revenue will increase, intention to pay a bigger month-to-month quantity till the mortgage is eradicated. Utilizing a scholar mortgage calculator may also help make your purpose attainable.

Enhance Your Credit score Rating

An excellent credit score rating makes it simpler to satisfy quite a few private monetary objectives. You may get permitted for a greater residence or obtain a greater rate of interest in your automotive mortgage and mortgage funds. Though it is determined by the scoring system, aiming for a credit score rating above 700 will usually provide you with extra favorable phrases.

Methods to enhance your credit score rating embrace:

- Paying your lease on time and never breaking the lease early

- Utilizing 30 % (or much less) of your whole credit score restrict

- Paying your bank cards in full every month

- Holding outdated traces of credit score open

- Limiting the variety of laborious inquiries into your credit score

- Settling any delinquencies

Set a Retirement Date

In your 20s, you might need had a common thought of whenever you wished to retire. In your 30s, it’s time to consider a exact date that you could plan round. Your potential retirement 12 months will differ primarily based in your revenue, money owed, and private commitments.

For those who have been unable to stay to the objectives you made in your 20s, then it’s possible you’ll want to regulate your monetary planning for retirement to one thing extra attainable. If you’re dedicated to retiring in a selected 12 months, it’s possible you’ll must ramp up your financial savings and reduce pointless purchases. Figuring out when your mortgage might be paid off and when your youngsters might be completed with college also can have an effect on your retirement date.

Create a Final Will and Testomony

A final will and testomony is the authorized doc used to allocate your property after you die. It additionally identifies the executor of your property—the particular person liable for settling your excellent money owed and seeing that your will is honored.

With no will, your property might be distributed by the federal government after you die. This generally is a expensive course of with no assure that your needs might be honored. When you have plans for who inherits your belongings, assembly with an property planning lawyer must be made a precedence.

Lengthy-Time period Monetary Objectives For Your 40s

Life in your 40s is stuffed with tasks. You seemingly personal extra property now than at another time in your life, your loved ones is rising, and your objectives are altering. Now it’s time to reorient your long-term monetary objectives to your present scenario.

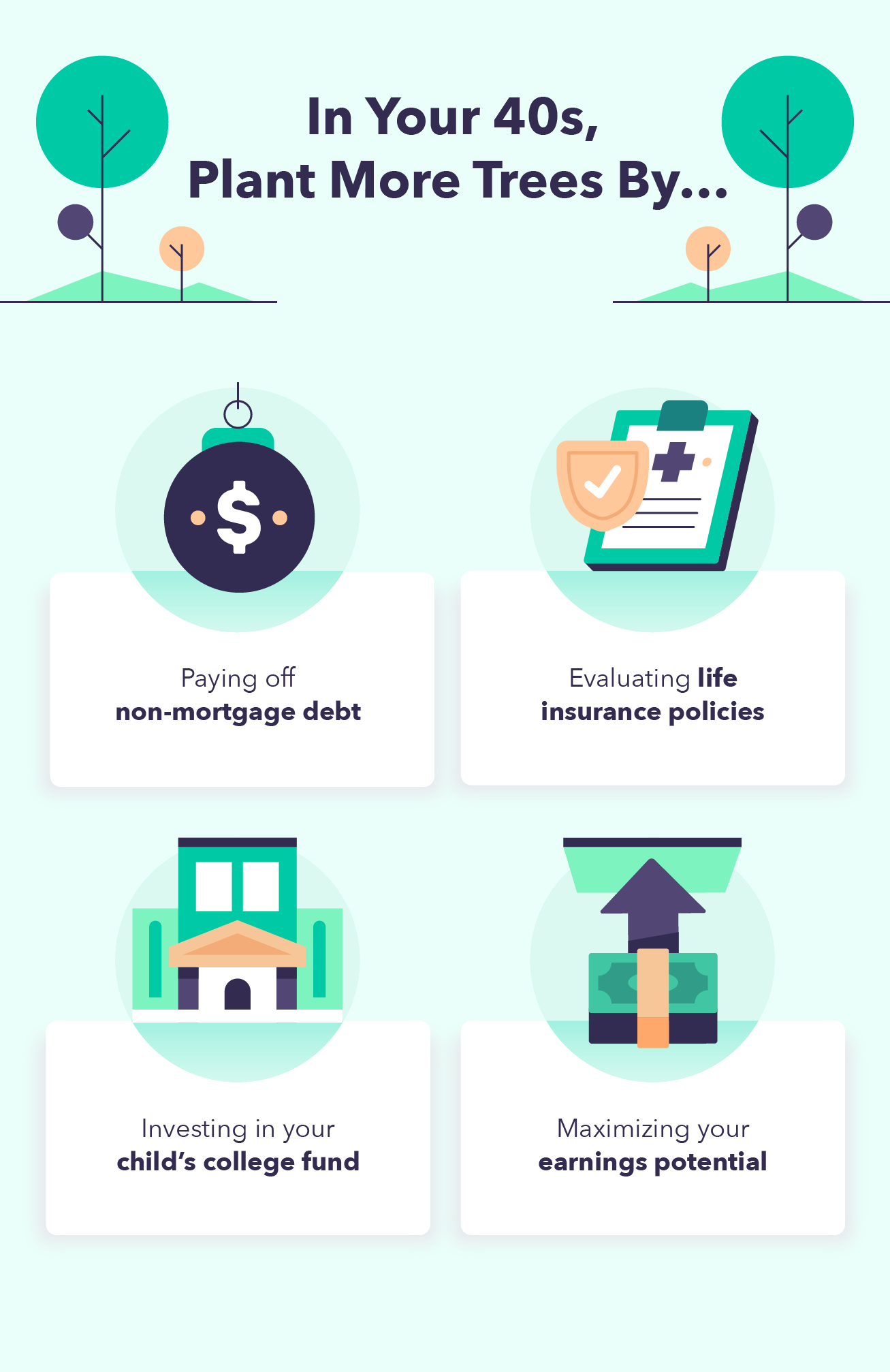

Pay Off Non-Mortgage Debt

Apart out of your mortgage, which might observe you into your 50s and 60s, all different debt elimination must be prioritized. Simply since you eradicated some money owed in your 20s and 30s doesn’t imply new money owed haven’t appeared.

You might have new bank card debt or scholar loans from returning to highschool. Car purchases can occur at any level in life. Whatever the purpose for the debt, you gained’t need excessive APR funds lingering when you’re approaching retirement age.

Consider Life Insurance coverage Insurance policies

Life insurance coverage is what your dependents will use to bolster their way of life within the occasion of your demise. Having a complete coverage can guarantee their wants are met even when your financial savings at the moment aren’t sufficient.

Because of the monetary obligations the typical 40-year-old has, it’s typically really useful to buy extra life insurance coverage than you initially thought you’d want. You’ll wish to be sure your loved ones can cowl their dwelling bills and settle any money owed with out your revenue.

Put money into Your Youngster’s School Fund

Saving to your youngsters’s schooling is among the greatest methods to set them up for monetary success. If they will keep away from the early debt of scholar loans, then they will deal with different monetary objectives earlier.

A school fund is a big funding and it’ll take a very long time to perform. Relying on when you’ve gotten youngsters, it’s possible you’ll wish to begin their faculty fund earlier than your 40s to make sure it’s sufficient by the point they graduate highschool.

Maximize Your Earnings Potential

Most individuals attain their peak incomes potential in some unspecified time in the future of their 40s. Placing your self ready to maximise this quantity will set the stage to your high quality of life in retirement. A bigger revenue will allow you to max out your retirement contributions.

That is one other time to research in case your present job aligns together with your long-term monetary plans or if it’s essential make a change. Search for methods to earn more money by negotiating for a increase, incomes a promotion, beginning a aspect hustle, or altering employers.

Lengthy-Time period Monetary Objectives For Your 50s and 60s

These twenty years in an individual’s life typically have a big diploma of overlap. Your private commitments are simplified, and your set retirement date is lastly inside view. All that’s left so that you can do is tie up free ends.

Change into Fully Debt-Free

Paying off your mortgage is a significant monetary purpose and getting it carried out earlier than you retire is a big accomplishment. Knocking it out when you’re nonetheless working full-time allows you to put more cash into your retirement portfolio. The identical goes for another excellent money owed which can be persisting. These month-to-month bills can extend your time within the workforce previous what you initially supposed.

Plan Lengthy-Time period Care Choices

There could come a time in your life when you’re now not capable of deal with your self. You’ll desire a plan in place earlier than that occurs so your funds might be sufficient to satisfy your wants. Make sure that your loved ones is conscious of your needs to allow them to put together as effectively. Some issues to think about embrace:

- Who might be your guardian?

- Will you obtain in-home care or transfer to a live-in facility?

- For those who require a live-in facility, which one will it’s?

Lengthy-term care providers are a expensive addition to your retirement price range. Organising funding for such an occasion years earlier than the necessity arises could make it extra manageable.

Re-evaluate Your Property

Many adjustments could have occurred in your life because you first drafted your will. Re-evaluating what property are presently in your possession will make the method of managing your property go a lot smoother. That is one other alternative to debate your monetary affairs and desires with your loved ones. Keep away from sudden revelations after your demise, so there isn’t combating amongst your family members.

Downsize Your Residing Bills

Implementing cost-cutting measures in your life earlier than retirement may also help put your future way of life into perspective. Chances are you’ll understand that your preliminary retirement price range can’t meet your wants and also you want extra time to save lots of.

The home you raised a household in could now not be needed as soon as your youngsters are out of the home. Promoting it for a smaller property can add to your financial savings whereas lowering bills. The identical might be stated for proudly owning a number of autos or trip properties.

Everybody has distinctive wants and obligations that affect their monetary journey. Budgeting and saving can preserve you on observe to satisfy your long-term monetary objectives. No matter the place your funds stand at the moment, it’s all the time a good time to organize for a lot of of life’s necessary occasions.