Blink and also you missed it, however the yield on the 2-year Treasury word traded briefly above the yield on the 10-year word Tuesday afternoon, briefly inverting the yield curve and triggering recession warning bells.

Information exhibits that it hasn’t paid prior to now to desert shares the second the Treasury yield curve turns the wrong way up, with quick time period yields greater than long term yields.

Not a very good timing instrument

“Whereas a very good indicator of future financial woes, an inverted yield curve has not been an excellent timing instrument for fairness buyers,” wrote Brian Levitt, world market strategist at Invesco in a March 24 word.

See: A key a part of the Treasury yield curve has lastly inverted, setting off recession warning — right here’s what buyers have to know

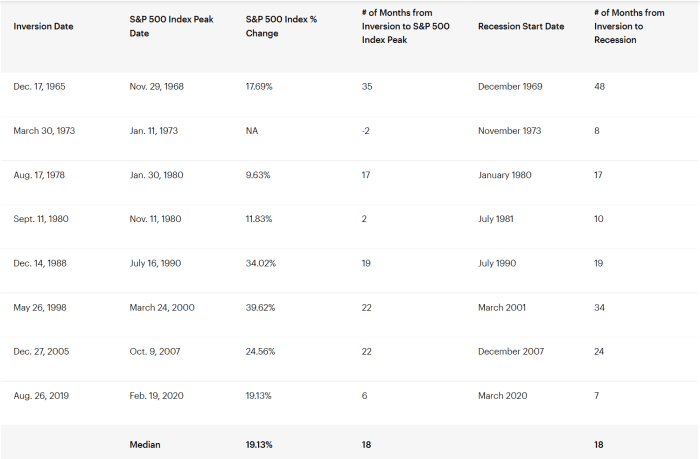

“For instance, buyers who bought when the yield curve first inverted on Dec. 14, 1988, missed a subsequent 34% acquire within the S&P 500 index,” Levitt wrote. “Those that bought when it occurred once more on Might 26, 1998, missed out on 39% extra upside to the market,” he mentioned. “Actually, the median return of the S&P 500 index from the date in every cycle when the yield curve inverts to the market peak is nineteen%.” (See desk under.)

Invesco

Traders definitely didn’t head for the hills Tuesday. U.S. shares ended with robust good points, constructing on a bounce from early March lows and even propelling the S&P 500

SPX,

to an exit from the market correction it entered in February. The Dow Jones Industrial Common

DJIA,

jumped 338 factors, or 1%, whereas the Nasdaq Composite

COMP,

superior 1.8%.

Learn: S&P 500 exits correction: Right here’s what historical past says occurs subsequent to U.S. stock-market benchmark

Inversions and what they imply

Usually the yield curve, a line that measures the yields throughout all maturities, slopes upward given the time worth of cash. An inversion of the curve indicators that buyers anticipate long term charges to be under near-term charges, a phenomenon broadly taken as a sign of a possible financial downturn.

However there’s a lag there, too. Levitt famous that the information, going again to 1965, present the median size of time between an inversion and a recession has been 18 months — matching the median stretch between the onset of an inversion and an S&P 500 peak.

Furthermore, researchers have argued {that a} persistent inversion is important to ship a sign, one thing that hasn’t occurred but, however stays broadly anticipated.

Which curve?

An inversion of the 2-year

TMUBMUSD02Y,

/10-year

TMUBMUSD10Y,

measure of the yield curve has preceded all six recessions since 1978, with only one false constructive, mentioned Ross Mayfield, funding technique analyst at Baird, in a Monday word.

However the 3-month/10-year unfold is seen as even, if solely barely, extra dependable and has been extra fashionable amongst teachers, famous researchers on the San Francisco Fed. And Fed Chairman Jerome Powell earlier this month expressed a choice for a extra short-term oriented measure that measures 3-month charges versus expectations for 3-month charges 18 months sooner or later.

The three-month/10-year unfold, in the meantime, is “removed from inverted,” Mayfield famous.

See: Inventory-market buyers ought to watch this a part of the yield curve for the ‘greatest main indicator of hassle forward’

Certainly, the divergence between the 2 carefully adopted measures of the curve has been a head scratcher for some market watchers.

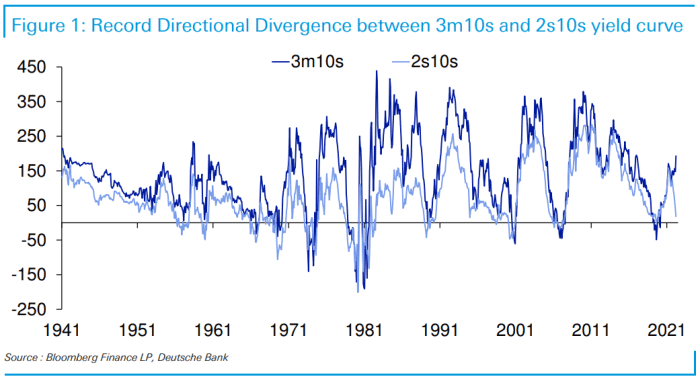

“The exceptional factor is that the 2 have all the time gone hand in hand directionally till round December 2021 when 3m/10s began to steepen as 2s/10s collapsed,” mentioned Jim Reid, strategist at Deutsche Financial institution, in a Tuesday word (see chart under).

Deutsche Financial institution

“There has by no means been such a directional divergence probably as a result of the Fed [has] by no means been as behind the ‘curve’ as they’re immediately,” Reid mentioned. “If market pricing is appropriate, they’ll quickly catch up over the subsequent yr so it’s doable that in 12 months’ time” the 3-month/10-year measure shall be flat as short-term charges rise because the Fed hikes its benchmark coverage charges.

The takeaway, Mayfield wrote, is that the yield curve stays a strong indicator and is on the very least signaling a cooling financial system.

“Volatility ought to stay heightened and the bar for investing success is raised. However ultimately, we predict it’s price taking the time to digest the bigger image and never depend on any single indicator,” he mentioned.

In One Chart: ‘The dam lastly broke’: 10-year Treasury yields spike to breach prime of downward pattern channel seen since mid-Nineteen Eighties