Value Of Items Bought Definition

Value of products bought (COGS) is the price of producing the products bought by an organization. It accounts for the price of supplies and labor immediately associated to that good and for a delegated accounting interval.

As an organization promoting merchandise, you have to know the prices of making these merchandise. That’s the place the price of items bought (COGS) method is available in. Past calculating the prices to supply a great, the COGS method can even unveil profits for an accounting interval, if value adjustments are crucial, or whether or not you have to reduce down on manufacturing prices.

Whether or not you fancy your self as a business owner or a shopper or each, understanding tips on how to calculate value of products bought can assist you’re feeling extra knowledgeable concerning the merchandise you’re buying — or producing.

What Is Value of Items Bought?

Value of products bought is the price of producing the products bought by an organization. It consists of the price of supplies and labor immediately associated to that good. Nonetheless, it excludes oblique bills equivalent to distribution and gross sales pressure prices.

What Is the Value of Items Bought System?

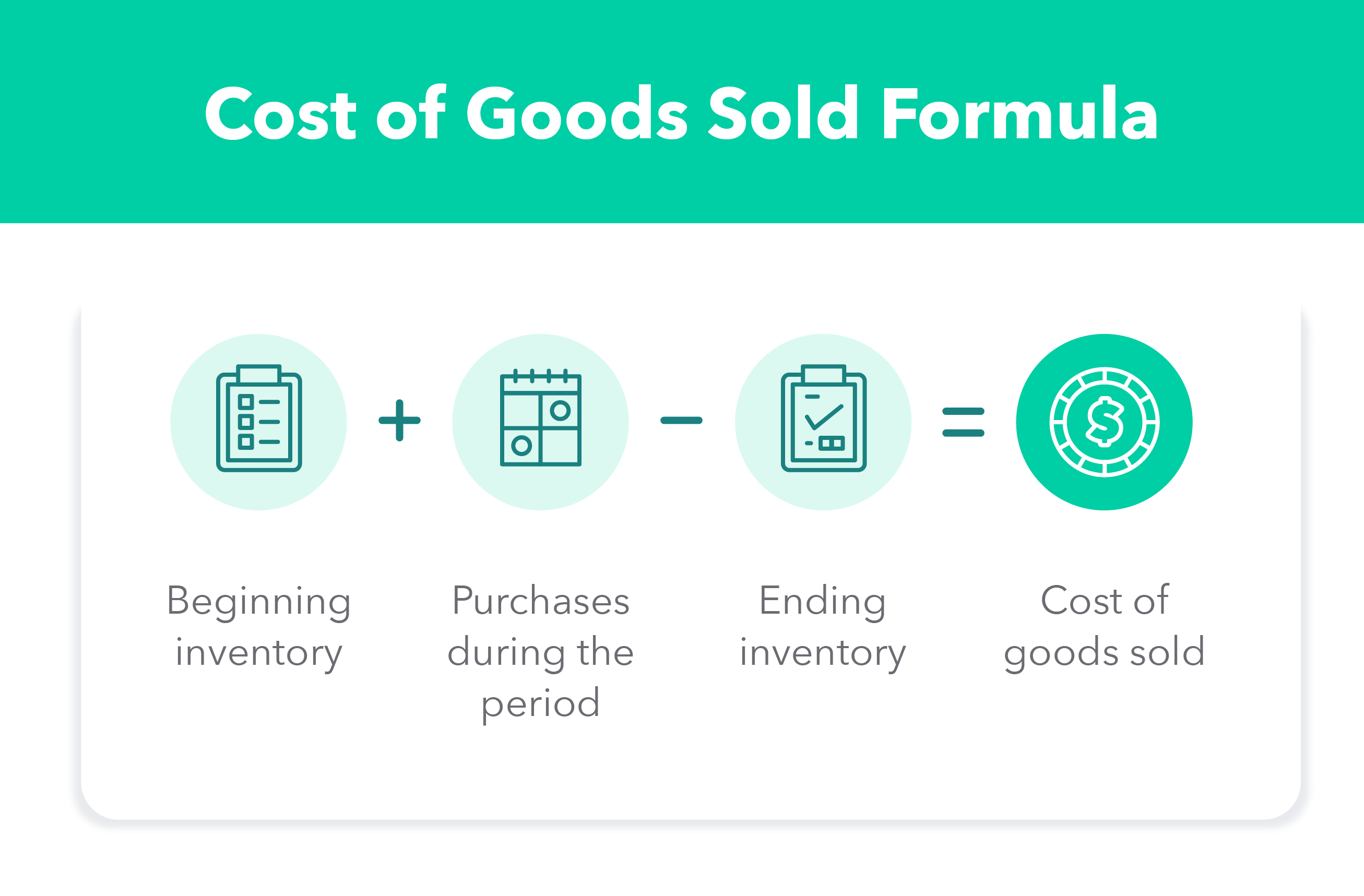

When selling a product, you have to perceive the manufacturing prices related to it in a given interval, which might be a month, quarter, or 12 months. You are able to do that through the use of the price of items bought method. It’s an easy calculation that accounts for the start and ending stock, and purchases throughout the accounting interval. Right here is an easy breakdown of the price of items bought method:

| COGS = starting stock + purchases throughout the interval – ending stock |

How Do You Calculate Value of Items Bought?

To calculate value of products bought, you need to decide your starting stock — that means your merchandise, together with uncooked supplies and provides, for example — at the start of your accounting period. Then add within the new stock bought throughout that interval and subtract the ending stock — that means the stock leftover on the finish in your accounting interval. The prolonged COGS method additionally accounts for returns, allowances, reductions, and freight expenses, however we’re sticking to the fundamentals on this clarification.

Taking it one step at a time can assist you perceive the COGS method and discover the true value behind the products being bought. Right here is the way you do it:

Step 1: Determine Direct and Oblique Prices

Whether or not you manufacture or resell merchandise, the COGS method means that you can deduct the entire prices related to them. Step one is to distinguish the direct prices, that are included within the COGS calculation, from oblique prices, which aren’t.

Direct Prices

Direct prices are the prices tied to the manufacturing or buy of a product. These prices can fluctuate relying on the manufacturing degree. Listed below are some direct prices examples:

- Direct labor

- Direct supplies

- Manufacturing provides

- Gas consumption

- Energy consumption

- Manufacturing workers wages

Oblique Prices

Oblique prices transcend prices tied to the manufacturing of a product. They embody the prices concerned in sustaining and working the corporate. There might be fastened oblique prices, equivalent to hire, and fluctuating prices, equivalent to electrical energy. Oblique prices usually are not included within the COGS calculation. Listed below are some examples:

- Utilities

- Advertising campaigns

- Workplace provides

- Accounting and payroll providers

- Insurance coverage prices

- Worker advantages and perks

Step 2: Decide Starting Stock

Now it’s time to find out your starting stock. The start stock would be the quantity of stock leftover from the earlier time interval, which might be a month, quarter, or 12 months. Starting stock is your merchandise, together with uncooked supplies, provides, and completed and unfinished merchandise that weren’t bought within the earlier interval.

Needless to say your starting stock value for that point interval needs to be precisely the identical because the ending stock from the earlier interval.

Step 3: Tally Up Gadgets Added to Your Stock

After figuring out your starting stock, you additionally must account for any stock purchases all through the interval. It’s essential to maintain observe of the price of cargo and manufacturing for every product, which provides to the stock prices throughout the interval.

Step 4: Decide Ending Stock

The ending stock is the price of merchandise leftover within the present interval. It may be decided by taking a bodily stock of merchandise or estimating that quantity. The ending stock prices will also be lowered if any stock is broken, out of date, or nugatory.

Step 5: Plug It Into the Value of Items Bought Equation

Now that you’ve got all the data to calculate value of products bought, all there’s left to do is plug it into the COGS method.

An Instance of The Value of Items Bought System

Let’s say you wish to calculate the price of items bought in a month-to-month interval. After accounting for the direct prices, you discover out that you’ve got a starting stock amounting to $30,000. All through the month, you buy an extra $5,000 value of stock. Lastly, after taking stock of the merchandise you could have on the finish of the month, you discover that there’s $2,000 value of ending stock.

Utilizing the price of items bought equation, you may plug these numbers in as such and uncover your value of products bought is $33,000:

| COGS = starting stock + purchases throughout the interval – ending stock |

| COGS = $30,000 + $5,000 – $2,000 |

Accounting for Value of Items Bought

There are totally different accounting strategies used to document the extent of stock throughout an accounting interval. The accounting methodology chosen can affect the worth of the price of items bought. The three primary strategies of accounting for the price of items bought are FIFO, LIFO, and the common value methodology.

FIFO: First In, First Out

The primary in, first out methodology, also referred to as FIFO, is when the earliest items that had been bought are bought first. Since merchandise costs have a tendency of going up, through the use of the FIFO methodology, the corporate could be promoting the least costly merchandise first. This interprets right into a decrease COGS in comparison with the LIFO methodology. On this case, the net income will enhance over time.

LIFO: Final In, First Out

The final in, first out methodology, also referred to as LIFO, is when the latest items added to the stock are bought first. If there’s an increase in costs, an organization utilizing the LIFO methodology could be primarily promoting the products with the very best value first. This results in the next COGS in comparison with the FIFO methodology. By utilizing this methodology, the online revenue tends to lower over time.

Common Value Technique

The common value methodology is when an organization makes use of the common value of all items in inventory to calculate the start and ending stock prices. Which means there will probably be much less of an impression within the COGS by larger prices when buying stock.

Issues for Value of Items Bought

When calculating value of products bought, there are a couple of different elements to think about.

COGS vs. Working Bills

Enterprise homeowners are seemingly accustomed to the time period “working bills.” Nonetheless, this shouldn’t be confused with the price of items bought. Though they’re each firm expenditures, working bills usually are not immediately tied to the manufacturing of products.

Working bills are oblique prices that hold an organization up and working, and may embody rent, gear, insurance coverage, salaries, advertising, and workplace provides.

COGS and Stock

The COGS calculation focuses on the stock of your small business. Stock might be objects bought or made your self, which is why manufacturing prices are solely typically thought of within the direct prices related together with your COGS.

Value of Income vs. COGS

One other factor to think about when calculating COGS is that it’s not the identical as value of income. Value of income takes into consideration a number of the oblique prices related to gross sales, equivalent to advertising and distribution, whereas COGS doesn’t take any oblique prices into consideration.

Exclusions From COGS Deduction

Since service firms would not have a listing to promote and COGS accounts for the price of stock, they’ll’t use COGS as a result of they don’t promote a product — they might as an alternative calculate the price of providers. Examples of service firms are accounting companies, legislation workplaces, consultants, and actual property appraisers.

The Backside Line

Operating a enterprise requires many transferring components. To make sure an organization is making a revenue and everybody’s paid a good salary, enterprise homeowners ought to have a well-rounded view of the prices related to their items bought. Following this step-by-step information to discover ways to use the price of items bought method is an efficient start line. As at all times, it’s essential to seek the advice of an skilled, equivalent to an accountant, when doing these calculations to verify all the things is accounted for.

Sources: QuickBooks